HARRY'S BI-WEEKLY UPDATE 1.8.25

January 8, 2025

HARRY’S BI-WEEKLY UPDATE

A Current Look at the Colorado Springs Residential real estate Market

As part of my “Special Brand of Customer Service”, it is my desire to share current Residential real estate issues that will help to make you a more successful and profitable Buyer and Seller.

HAPPY NEW YEAR….AND WELCOME TO 2025

As we begin 2025, I wish all of you a happy, healthy, and prosperous year.

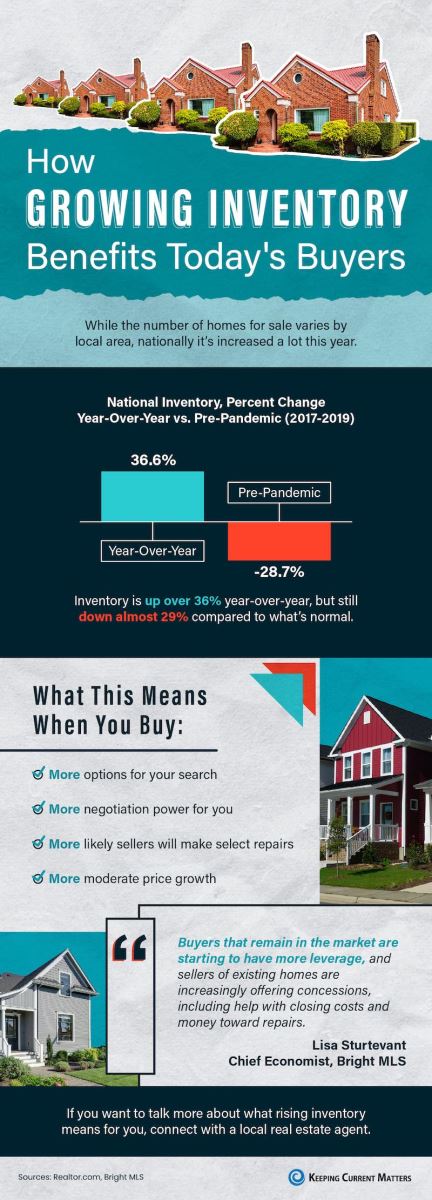

2024 was another year of trials and tribulations in the Residential real estate market, both nationally and here in Colorado Springs.

High interest rates and the lack of existing homes for sale created the slowest market year since 2011.

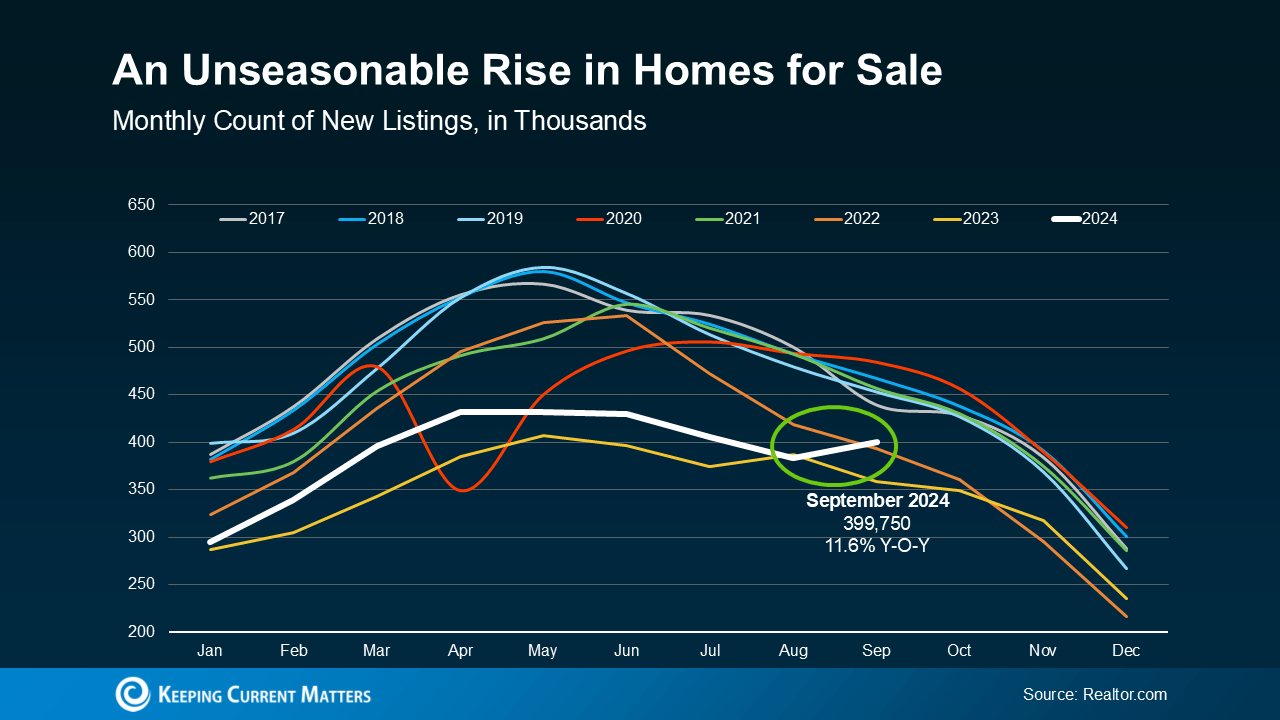

However, U.S. pending home sales hit a 21-month high in November and as you will see from the statistics below, our listings and sales are on the rise as well.

We are seeing more listings for this time of year than in the recent past and I believe it’s due to a more optimistic outlook that seems to be permeating the housing market. Folks are realizing that interest rates are not going back to the historic lows of 4 or 5 years ago and home prices are continuing to rise.

I always start my new year by predicting how I personally see the Residential real estate market affecting not only the Colorado Springs area, but also how it will affect my clients in general.

My predictions for 2025 include the expectation that things will continue to be slow in terms of time. It will take a bit longer to sell, and pricing adjustments might be necessary, but home values will still rise by 3% to 4%. Nothing is “black and white” anymore and anything is negotiable, even interest rates.

I also believe:

- Demand for existing homes will be strong due to lack of homes for sale.

- Interest rates on 30-year fixed-rate mortgages will drop down to the 6.2%-6.3% range by the end of 2025, which is great news since rates were as high as 7.75% in 2024.

- If homes are priced right, the probable number of days on the market will be around 60 days.

- Renters are going to continue to be looking to buy, if possible, due to higher rental rates.

- Homes will continue to appreciate as they have in the past, although not as rapidly. As I’ve said time and again, you can’t only look at the last quarter or even the last couple of years. real estate is a long-term investment.

When you look at the value of home ownership compared to other investments, it’s still going to be extremely positive. And even in a slow market as we’ve recently seen, our home values keep appreciating…although at a more “normalized” rate.

- For most, your home will likely continue to be your largest and fastest growing investment.

I have always said that no one can expect to buy at the lowest price point, nor sell at the highest. It just isn’t possible and most anyone who thinks they can will likely lose in the long run.

Yes, prices are holding steady and those who are waiting for them to drop before they buy will likely not see this happen. This is also reflected in the statistics below. You can see that homes are selling at close to listing price and home values are not depreciating.

And, while it may be more difficult today, it’s still possible for you to find what you need, want, and can afford in a home.

With new companies relocating here or expanding their current business plans, we are seeing an influx of folks moving here for jobs and they are needing places to live. This is putting even more pressure on folks wanting to buy—either to sell and trade up, purchase a first home or even for investment purposes.

Since sales have been picking up recently, during what is traditionally the slowest time of the year, it appears that folks are starting to buy and sell much earlier than normal. They aren’t waiting for the “traditional” spring buying and selling season.

It’s important to note that with rising competition, folks starting to buy and sell earlier than normal, and still so few existing homes for sale, if you are in the market you need to be prepared to know exactly what you want, need, and can afford PRIOR to beginning the search.

That’s where I come into the picture. The current market is not for the timid or inexperienced. It takes a lot of advanced planning and knowledge of how to navigate these waters.

My almost 53 years in the local residential real estate arena, coupled with my investment banking background, give me an edge that my clients have found to be crucial in helping them and their families realize their personal real estate visions.

A new year brings with it a lot of new hopes and dreams. If Residential real estate is among your hopes and dreams for 2025, please give me a call at 719.593.1000 or email me at Harry@HarrySalzman.com and let me help make them come true.

The earlier you begin the process, the earlier you will be realizing those dreams for you and your family.

And…if you’ve got two minutes and 24 seconds, I recommend that you take a look at my newest “crystal ball prediction” podcast . Simply click on the link below and you will be directed to my personal YouTube channel.

To watch, click here:

While you’re at it you might want to subscribe to my channel, so you won’t miss future broadcasts. It won’t cost you anything…well, it could cost you… if you miss some of my informative musings!

And now for statistics…

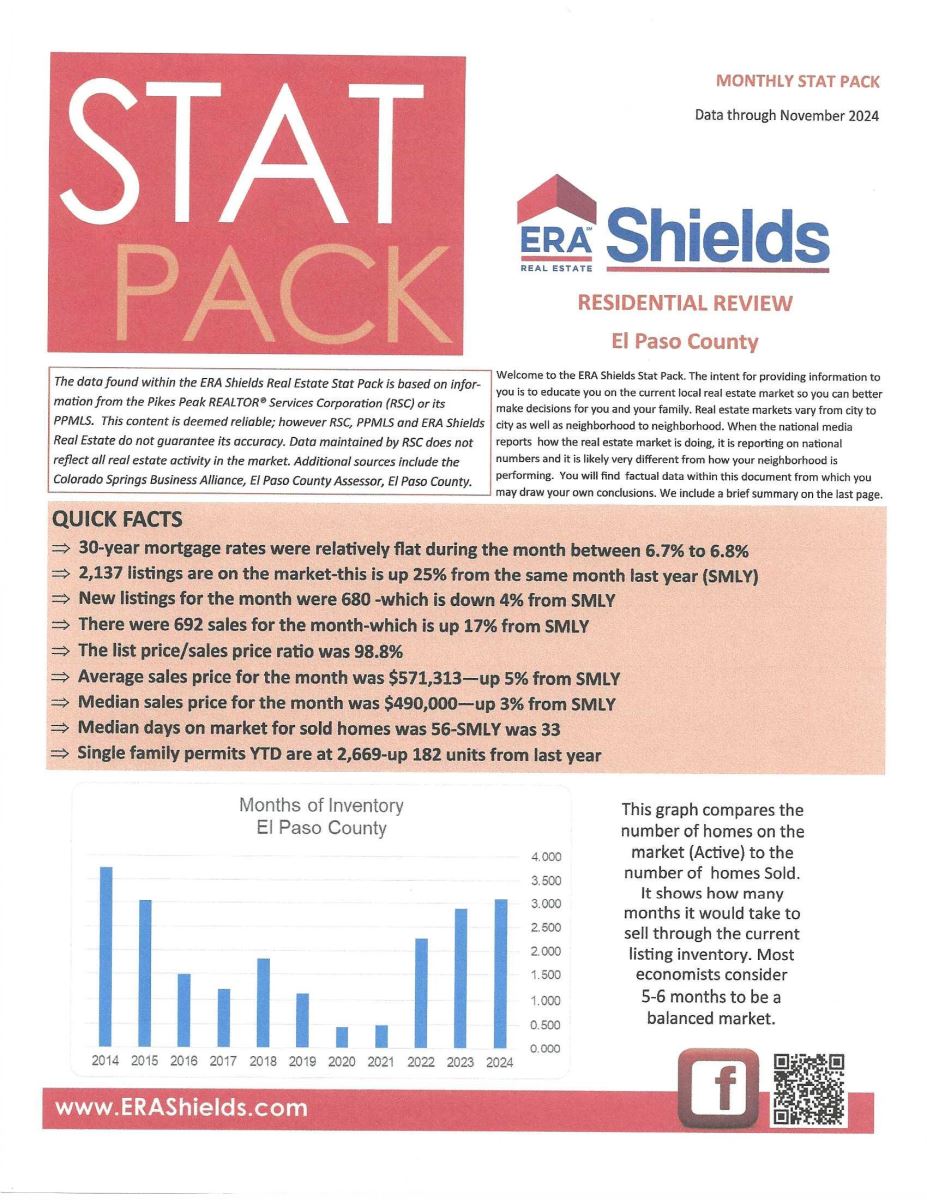

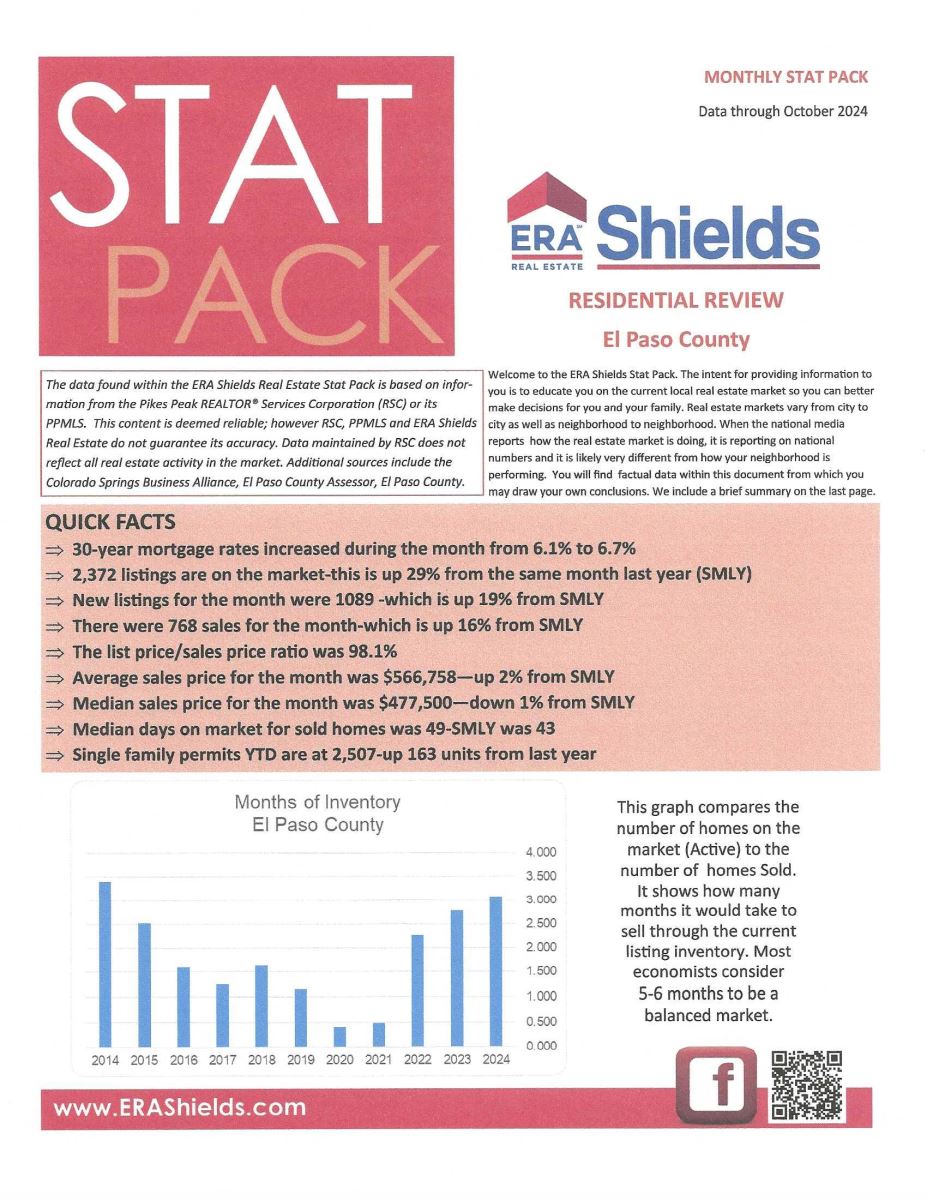

DECEMBER 2024

Statistics provided by the Pikes Peak REALTORS Service Corp., or it’s PPMLS

Here are some highlights from the December 2024 PPAR report:

In El Paso County, the average days on the market for single family/patio homes was 56. For condo/townhomes it was 63.

Also in El Paso County, the sales price/list price for single family/patio homes was 99.0% and for condo/townhomes it was 98.4%.

In Teller County, the average days on the market for single family/patio homes was 66 and the sales/list price was 97.5%.

Since these are year-end statistics, I am providing you with both the regularly posted year-over-year monthly stats as well as the cumulative year-to-date comparison of 2024 to 2023.

Please click here to view the detailed 10-page report, including charts. If you have any questions about the report or to find out how it relates to your individual situation, just give me a call.

In comparing December 2024 to December 2023 for All Homes in PPAR:

Single Family/Patio Homes:

· New Listings were 707, Up 22.5%

· Number of Sales were 877, Up 12.9%

· Average Sales Price was $545,969, Up 5.0%

· Median Sales Price was $485,000, Up 6.6%

· Total Active Listings are 2,505, Up 32.5%

· Months Supply is 2.9, Up 2.5%

Condo/Townhomes:

· New Listings were 116, Down 0.9%

· Number of Sales were 111, Down 2.6%

· Average Sales Price was $351,532, Down 1.0%

· Median Sales Price was $340,000, Up 3.0%

· Total Active Listings are 502, Up 62.5%

· Months Supply is 4.5, Down 23.7%

The Cumulative YTD Summary: (comparing Jan-Dec 2024 to Jan-Dec 2023)

Single Family/Patio Homes:

- New Listings were 16,173, Up 8.7%

- Sales were 11,503, Down 2.0%

- Average Sales Price was $549,346, Up 2.1%

- Volume was $6,319,127,038, Up 0.1%

Condo/Townhomes:

- New Listings were 2,660, Up 14.8%

- Sales were 1,695, Down 1.7%

- Average Sales Price was $368,540, Up 0.2%

- Volume was $624,675,300, Down 1.6%

Now a look at more statistics…

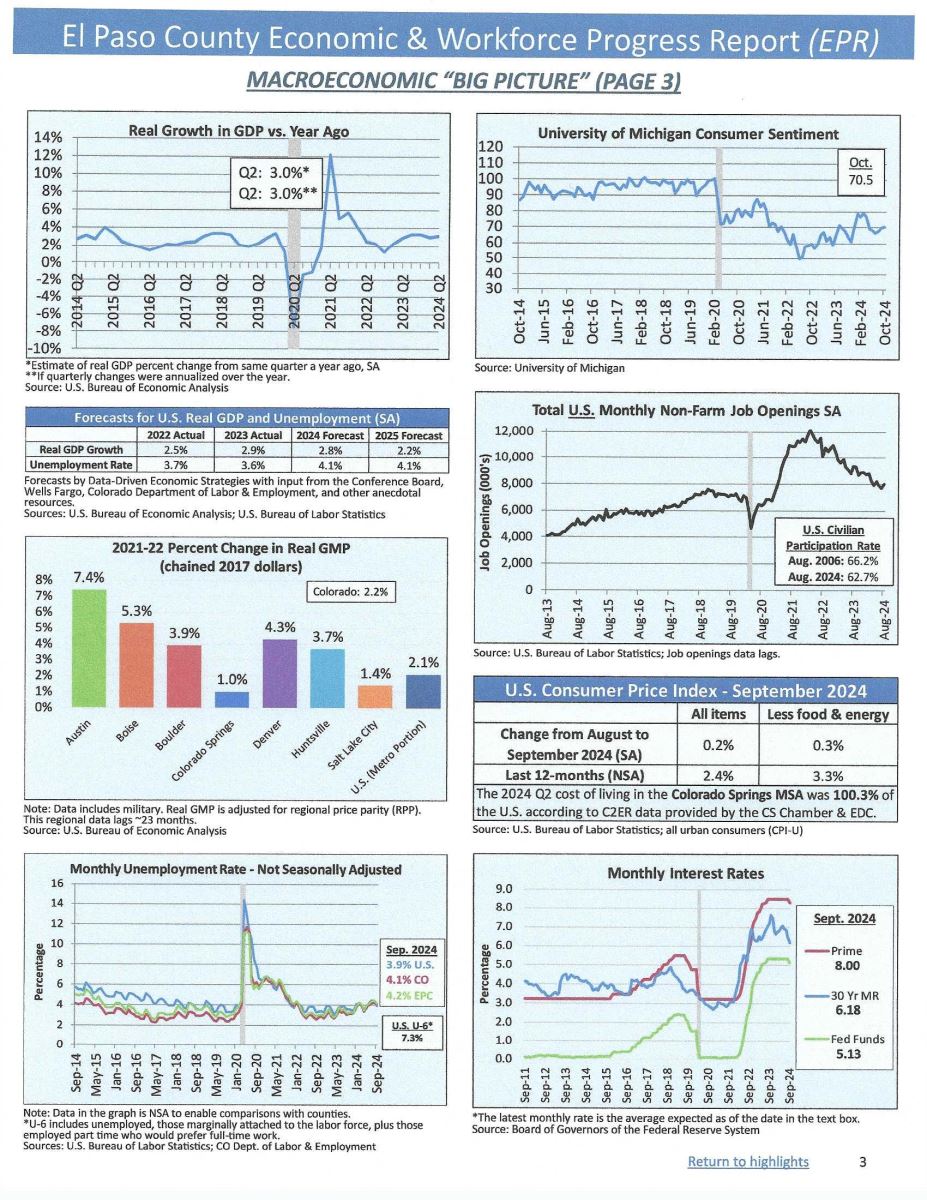

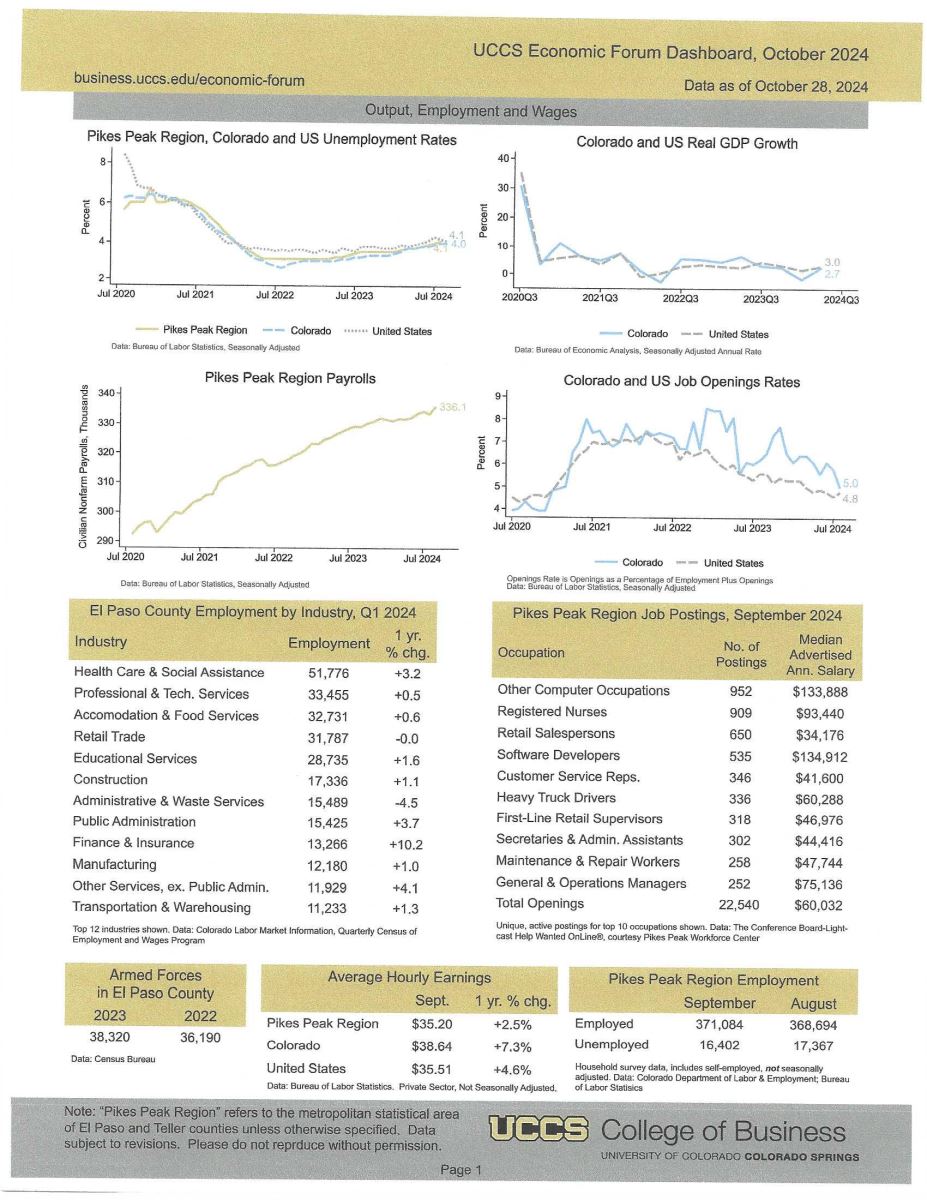

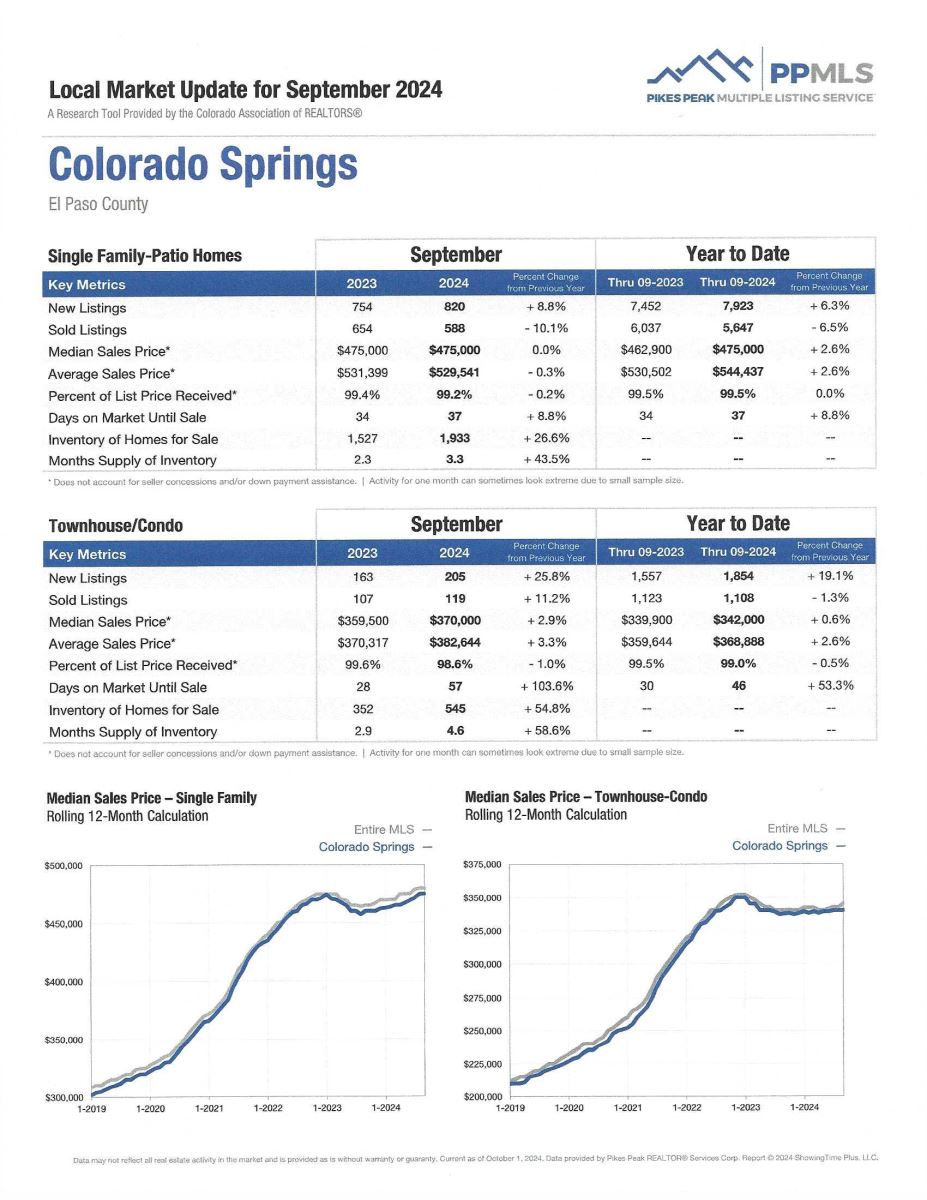

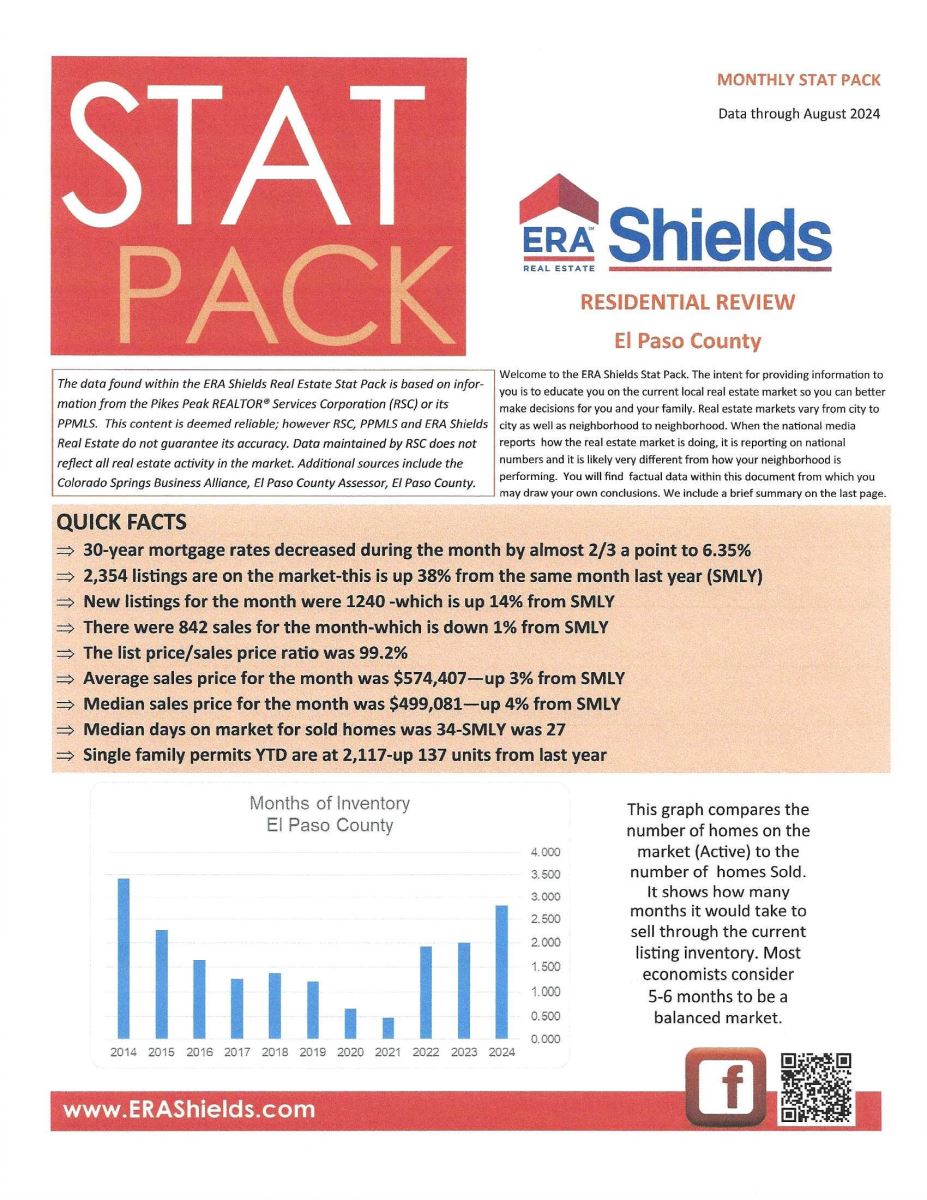

DECEMBER 2024 MONTHLY INDICATORS AND LOCAL MARKET UPDATE ILLUSTRATE OUR LOCAL TRENDS IN DETAIL

Colorado Association of REALTORS® , Pikes Peak REALTORS Service Corp, or it’s PPMLS

Providing greater detail than the above report, this contains information on both El Paso and Teller counties for Residential real estate.

The “Activity Snapshot” for all residential properties in El Paso and Teller counties shows the Year to Date one-year change:

- Sold Listings for All Properties were Up 15.5%

- Median Sales Price for All Properties was Up 5.9%

- Active Listings on All Properties were Up 25.5%

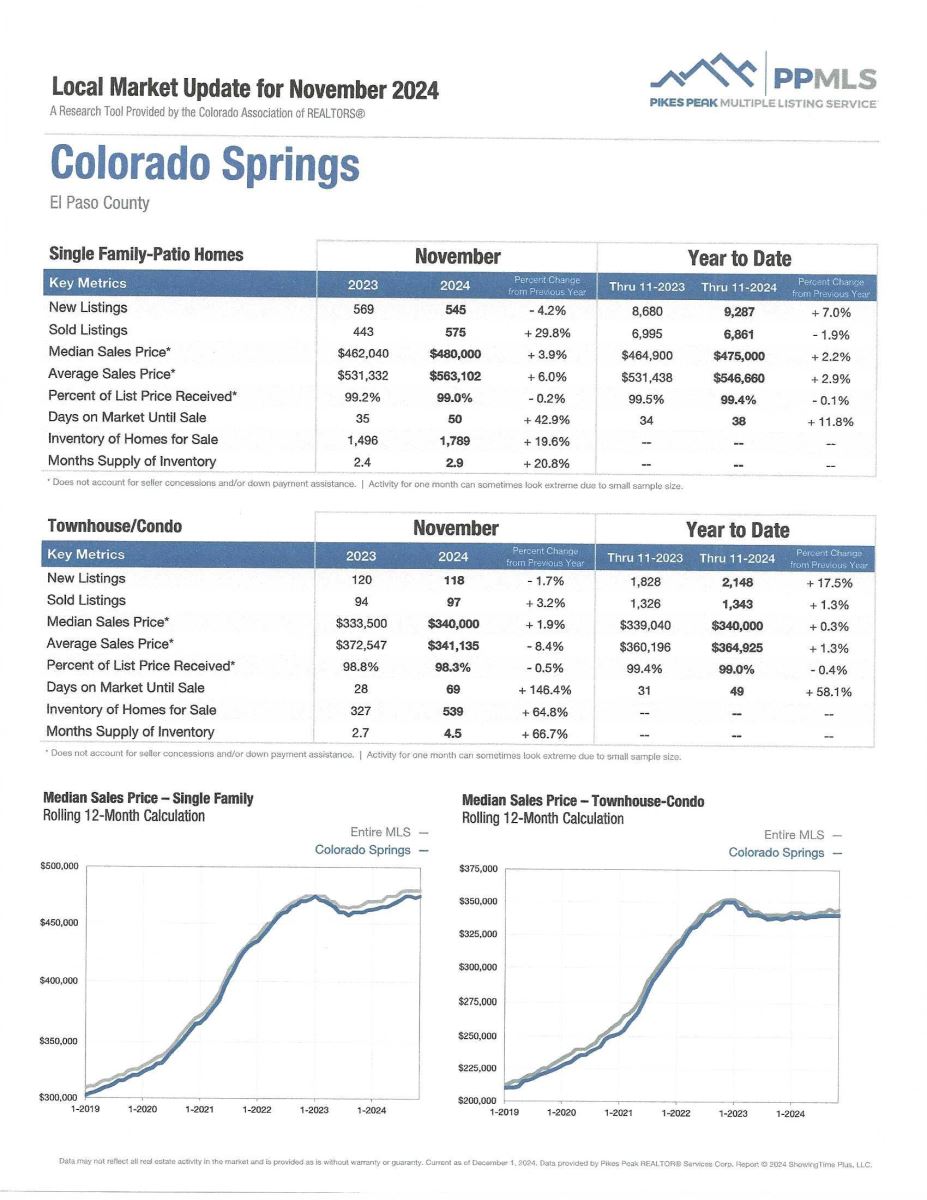

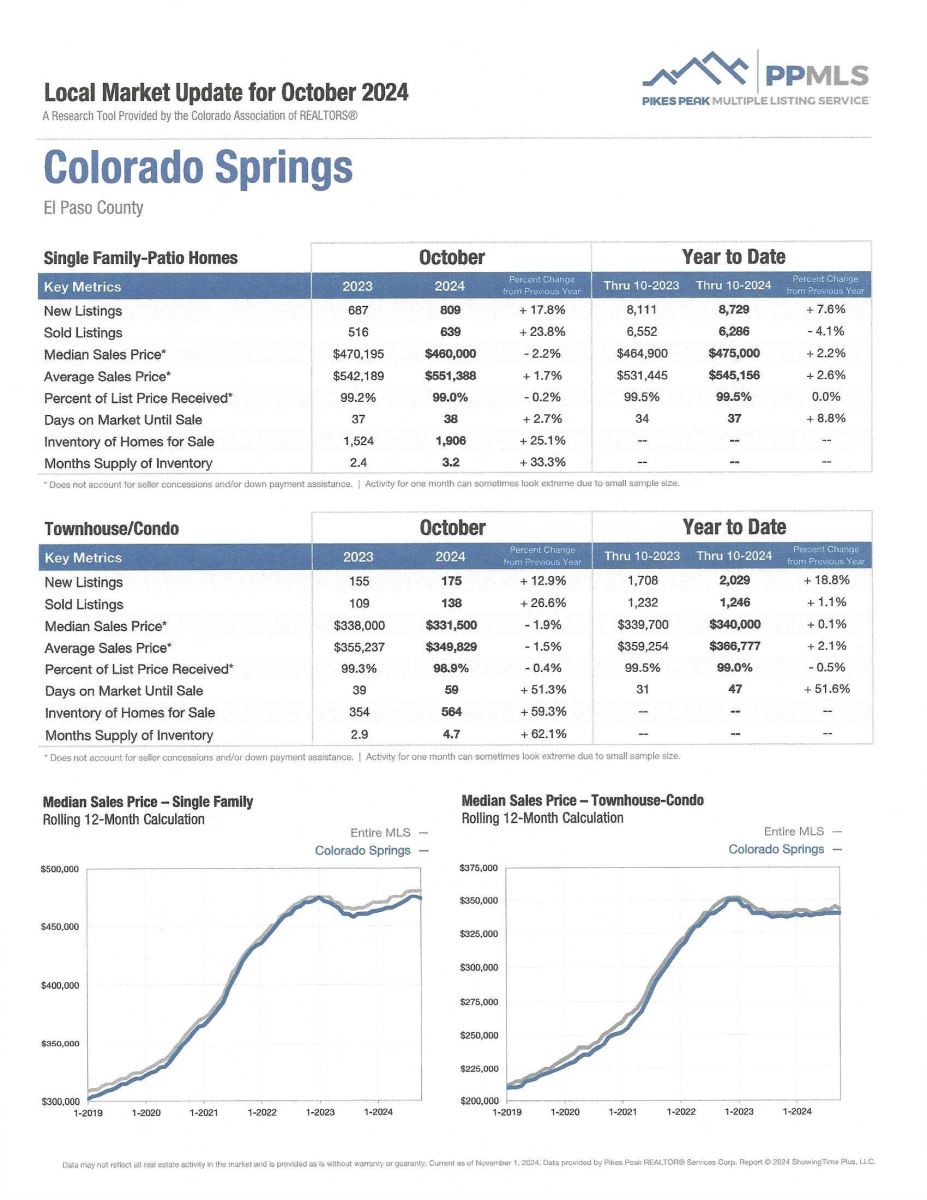

You can click here to read the 16-page Monthly Indicators or click here to get specific information on the geographical are of your choice from the 18-page Local Market Update. It’s a good idea to check out your own area or one that you might be considering in order to get a good idea of the local pulse. As an example, here is a detailed report on the Colorado Springs area:

.jpg)

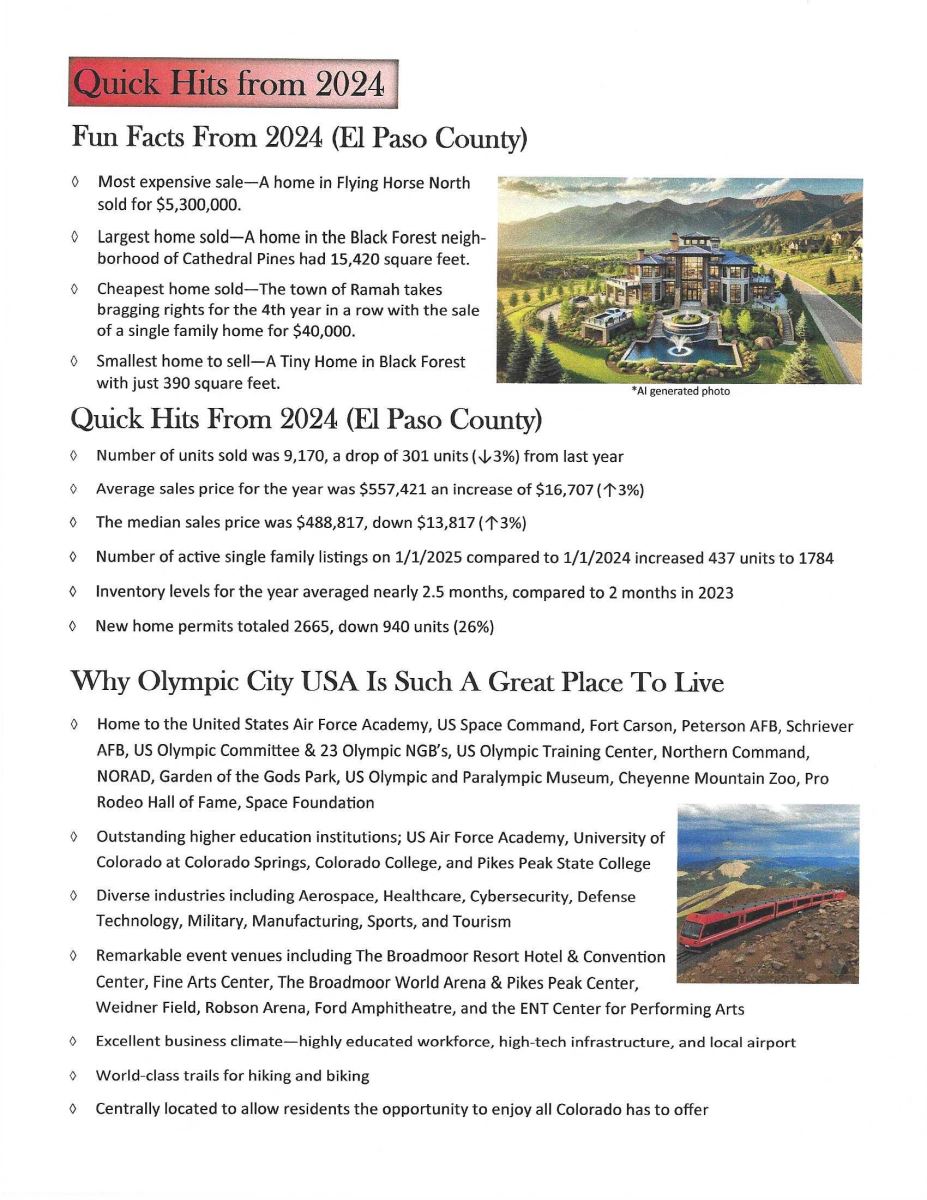

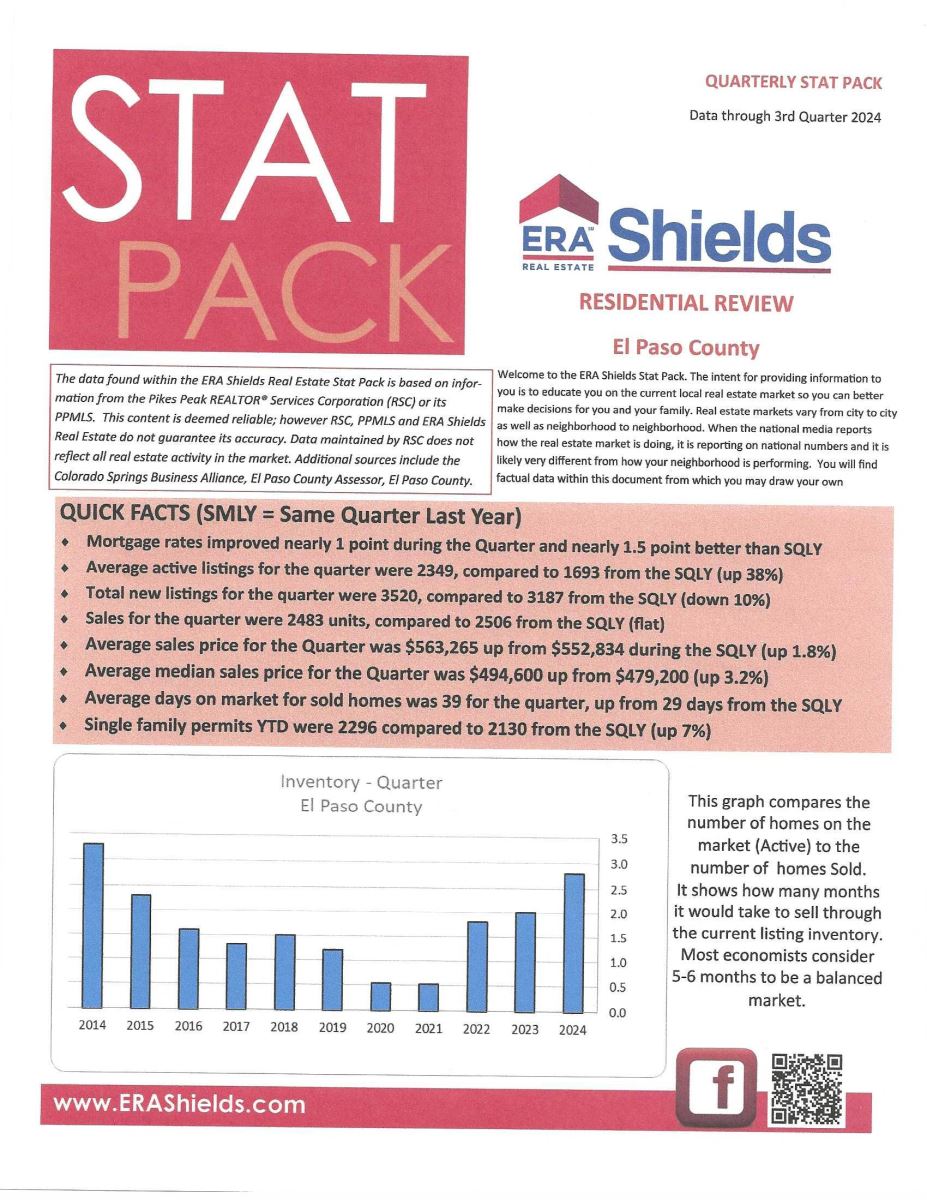

ERA SHIELDS 2024 RESIDENTIAL real estate REVIEW….AND A 2025 FORECAST

ERA Shields, January 2025

I am happy to share with you the “Colorado Springs Residential real estate 2024 Annual Review and 2025 Forecast” that is produced by my company. I believe you will find the information to be quite helpful and if you have any questions, you know where to reach me.

To read the report in its entirety please click here. I have reproduced several pages below.

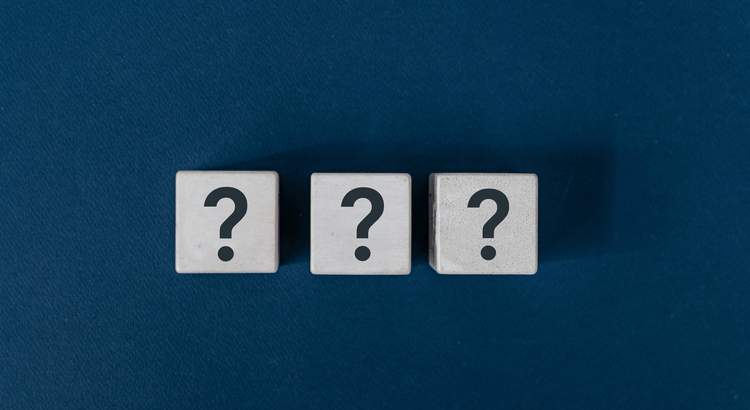

THE NATION’S HOTTEST housing market IN 2025? IT’S COLORADO SPRINGS SAYS A NEW FORECAST

The Gazette, 12.10.24

According to an annual forecast released in early December by Realor.com, Colorado Springs ranks as the nation’s No. 1 housing market for 2025 due to hefty increases in homes sales and prices.

Our top spot results from a 27.1% expected jump in the number of home sales in 2025 compared to 2024 and a 12.7% year-over-year predicted appreciation in prices. Combined, those two percentages gave the city the No. 1 ranking in the Realtor.com forecast for this year.

However, nice as all that sounds, I, among many local professionals, do not agree with that, especially since we have not seen that type of appreciation since the heydays of 2022 when interest rates had fallen to 3% and below.

Also, with so few available existing homes for sale, it’s not likely we would see such a percentage jump at present.

Lawrence Yun, chief economist for the National Association of Realtors (NAR) predicted in December that homes sales nationally would rise by about 10% in 2025 and prices would increase by just 2%. It’s quite doubtful that Colorado Springs is going to significantly exceed those predictions.

However, Realtor.com is sticking with those predictions. Ralph McLaughlin, senior economist for Realtor.com said via email, “While we don’t have a history of commenting on others’ opinions of our forecast, our models suggest that Colorado Springs is poised to be an overperformer in the housing market in 2025”.

Well…I can only say…let’s hope he’s even close to right, but certainly not count on it.

.jpg)

.png)

.jpg)

{kind=link}