May 23, 2011

HARRY’S WEEKLY UPDATE

A CURRENT LOOK AT THE COLORADO SPRINGS RESIDENTAIL real estate MARKET

NOTES FROM VEGAS

Well, it’s great to get back home.

The best way to appreciate our wonderful city is to visit somewhere else. Las Vegas was exciting, but Colorado Springs is heaven !!!

This year’s meeting of the “Worldwide ERC, the Workforce Mobility Association” had almost 2000 attendees and featured speakers from companies representing every aspect of the relocation industry. It was a great opportunity to hear what the “big boys” are saying about the economy and about the outlook for the future. It certainly gave us the opportunity to see how Colorado Springs stacks up against the rest of the country…..and believe me, we are looking very good, compared to most other cities in the U.S.

We have attended every one of these conferences since 1977 and, this year we were the only Realtor, or Broker/Owner from Colorado Springs in attendance.

Here are some of the significant changes that our weak economy is producing, as pointed out by many of the speakers at the conference:

- There has been a huge increase in the number of renters ….families who have lost their homes and their credit ratings because of foreclosure (Investors, take note!)

- More employees are turning down promotion opportunities which would require them to relocate. They can’t afford to take the loss in equity that selling their present home would require.

- More companies are cutting back on subsidizing the cost of relocating employees, except for their top executives. This makes it difficult for companies to offer their employees upward mobility within the company.

- It is not unusual for homes in some areas of a given city to take over a year to sell.

- real estate prices in most cities in the U.S. have not “bottomed out” yet.

- Colorado Springs is showing better numbers than approximately 60% - 70% of other cities nationwide.

The bottom line for Transferees is that they face a difficult choice in today’s market …Sell their present home at a loss, or, turn down the opportunity to advance within their company (and, as we all know, the opportunity to advance within a company is usually offered only once).

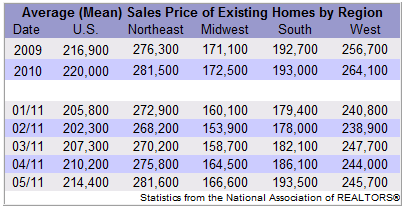

To bring the numbers into focus for our city, we see that, according to the latest statistics published by the Pikes Peak Association of Realtors, our average sales price for the past 4 months is up 1.1% over the same period last year. Admittedly, that’s not much of an increase, but it’s better than the situation in most other cites, which are still showing losses. In fact, according to Fiserv and Moody’s survey, the national U.S. home price average will show a 3 percent decline in the first half of this year. (See the following article, “Turnaround: 4 Months and Counting).

TURNAROUND: 4 MONTHS AND COUNTING?

The latest prediction from the authoritative Moody’s Analytics and Fiserv, Inc, which tracks home price trends in 375 U.S. markets, is that the national residential market is stabilizing, but will still show a 3% decline in the first half of this year. This is quite a different story from our local increase of 1.1% for the first quarter of 2011. Compared with other parts of the country, we’re doing great !!!

The survey also predicts that prices in the hardest-hit markets will take until the end of 2012 to level out.

Relative to household income, affordability is at or close to pre-bubble levels in nearly every metro area across the U.S. This dynamic, combined with growing economic strength, leads Fiserv and Moody’s Analytics to project that average U.S. home prices will stabilize in the third quarter of this year.

Even as balance returns to the housing market, the survey data forecasts the pace of recovery will be uneven across U.S. metro areas.

Although our local market is recovering at a good pace, there is still a great opportunity for Investors to build their investments by purchasing rental property. A larger pool of prospective Renters, plus the tightening credit requirements which make it difficult for former- home-owners to qualify for financing, plus the record-low cost of homes, plus the low interest rates which are still available, all combine to make rental properties a great investment.

To explore how investment properties might enhance your financial future, call us at 598-3200,or,1-800-677-MOVE(6683)

HERE’S ANOTHER PIECE OF GOOD NEWS FOR COLORADO SPRINGS

The Business section of the Gazette on Friday featured the story, “LOCAL JOBLESS RATE DIVES FOR SECOND STRAIGHT MONTH”.

The area’s jobless rate fell to 9.2% in April, from 9.7% the month before, the state Department of Labor and Employment reported Friday. That drop matched the one in March, when the jobless rate fell to 9.7% from a revised 10.2% in February.

The local job market is still struggling, but is showing improvement with 3,100 fewer people unemployed since January, despite a small increase in the labor force during the same period, said Fred Crowley, senior economist for the Southern Colorado Economic Forum.

All the numbers show that we’re a heck of a lot better off than most other parts of the country …..and we don’t have any problems that won’t be solved by JOBS, JOBS, JOBS.

Looks like our new mayor has his job cut out for him.

MORTGAGE RATES REACH ANOTHER LOW FOR 2011

For the fifth straight week, mortgage rates inched down again--this time reaching the lowest level of the year as well as lowest year-to-date. The 30-year fixed-rate mortgage averaged 4.61 percent this week, while the 15-year rate averaged 3.80 percent, Freddie Mac reports in its weekly mortgage market survey.

The 30-year mortgage hasn’t reached 4.61 percent or below since December 2010. Last year at this time, it averaged 4.84 percent while the 15-year fixed-rate mortgage averaged 4.24 percent.

The falling rates may be yet another lure to buyers during real estate’s traditionally prime home buying season. Owning a home has also recently been found to be more affordable than renting in 78 percent of the major U.S. cities, according to the latest data from Trulia.

WHERE ARE MORTGAGE RATES HEADED?

We often talk about the COST of buying a house vs. the PRICE of the home. The price obviously is a major component of the cost. The other major component is the interest rate on your mortgage. A small hike in mortgage interest rate can have a dramatic impact on your monthly payment. For that reason we try to keep you current on what is projected for rates in the future.

Four major institutions project rates: The National Association of Realtors (NAR), Fannie Mae, Freddie Mac and PMI. Here is what each is seeing in the next year.

By the Second Quarter of 2012:

- Fannie Mae predicts an interest rate of 5.6%

- PMI predicts an interest rate of 5.95%

- Freddie Mac predicts an interest rate of 5.6%

- NAR predicts an interest rate of 5.9%

Bottom Line

If you are looking to buy a house and are waiting to see what will happen with prices, remember interest rates will also impact your housing cost.

APRIL EXISTING-HOME SALES EASE

Existing-home sales slipped in April, although the market has managed six gains in the past nine months, according to the National Association of Realtors®.

Lawrence Yun, NAR chief economist, said the market is underperforming. “Given the great affordability conditions, job creation and pent-up demand, home sales should be stronger,” he said. “Although existing-home sales are expected to trend up unevenly through next year, unnecessarily tight credit is continuing to restrain the market, along with a steady level of low appraisals that result in contract cancellations.”

A parallel NAR practitioner survey shows 11 percent of Realtors® report a contract was cancelled in April from an appraisal coming in below the price negotiated between a buyer and seller, 10 percent had a contract delayed, and 14 percent said a contract was renegotiated to a lower sales price as a result of a low appraisal.

According to Freddie Mac, the national average commitment rate for a 30-year, conventional, fixed-rate mortgage was 4.84 percent in April, unchanged from March; the rate was 5.10 percent in April 2010.

“Although sales are clearly up from the cyclical lows of last summer, home sales are being held back 15 to 20 percent due to the very restrictive loan underwriting standards,” Yun said.

All-cash transactions stood at 31 percent in April, down from a record level of 35 percent in March; they were 26 percent in March 2010; investors account for the bulk of cash purchases.

NAR President Ron Phipps said the lending community needs to return to sensible standards. “We want to ensure that qualified buyers will be able to own their property on a sustained basis from a sound credit evaluation, but banks needn’t be so stingy as to only lend to those with the highest credit scores,” he said.

First-time buyers purchased 36 percent of homes in April, up from 33 percent in March; they were 49 percent in April 2010 when the tax credit was in place. Investors slipped to 20 percent in April from 22 percent of purchase activity in March; they were 15 percent in April 2010. The balance of sales was to repeat buyers, which were 44 percent in April.

Phipps added that proposals and regulations are being considered in Washington that could further constrain the housing market. “One of the most damaging proposals would effectively raise down-payment requirements to 20 percent, which would slam the brakes on the housing market,” he said. “What we need to do is simply return to the sound standards that were in place before the introduction of risky mortgage products.”

Ironically, low down-payment FHA and VA loans, which are so critical to this segment, have performed well and never needed a taxpayer bailout because those borrowers stayed well within their budgets.

NAR consumer survey data shows 56 percent of entry level buyers in the past year financed with an FHA loan.

BUYERS WANT MOVE-IN READY HOMES

Is a little elbow grease needed? Selling an "as-is" home may turn off buyers, according to a recent survey of real estate professionals.

The survey found that 87 percent of first-time buyers don't want to buy a home that requires them to do a lot of work; instead they want "move-in" ready. There's no doubt about it, a fixed-up home sells faster and agents say it sells for more money.

When contractor work totaled nearly $40,000, those repairs added more than $100,000 to the asking price! Of course, not all homes will require that amount of money and repairs. The point is putting a little effort, money, repairs, and tender loving care into it. This could go a long way at the time of the sale.

Repairing things like leaky pipes, broken windows, worn ceilings, as well as replacing old roofs and driveways can go a long way to help increase the listing price. Ripping up carpet and painting the inside and/or outside of the home can also increase buyer appeal.

real estate experts say the renovations don't need to be things like re-doing a kitchen or bath, unless it's tremendously outdated. The risk there is that sellers can put more into the renovation than they'll get out of it at the time of sale. Also, remodels to these areas of the home are quite personal and based heavily on personal taste.

What about clutter? Buyers often see clutter as a bigger issue than just a bunch of stuff strewn about the home. It can make them think that the home is more of a "project" house than it really is. Save yourself any issues and pack up your personal stuff.

Sometimes packing up stuff means storing big items that are cluttering the house. Borrow a friend's garage or rent a storage unit if your next home isn't ready. Unstuffing overly-furnished rooms can really open up the floor plan, allowing buyers to get a good idea of the size of the room.

Not preparing a home for sale can mean having to accept the very unwanted fact of listing it for a lower price.

ATLAS VAN LINES’ ANNUAL CORPORATE relocation SURVEY REFLECTS GROWING ECONOMIC OPTIMISM

After multiple years characterized by doubt and pessimism, relocation managers across the U.S. are expressing optimism that the worst of the recession is now in the rearview mirror. Responding to Atlas Van Lines’ 44th annual Corporate Relocation Survey, 72% of the relocation managers polled say they believe their respective companies will fare better in 2011. The optimism rate among large firms surveyed (more than 5,000 workers) jumps to 80%.

“Our relocation research has served as a solid barometer of where the American economy is headed,” said Jack Griffin, president and COO of Atlas World Group, the parent company of Atlas Van Lines. “The good news is that our survey respondents are focusing on growing their businesses and believe there will be abundant opportunity for expansion and increased revenues in 2011. This is encouraging for Atlas Van Lines and our relocation agents.”

Additional encouraging signs include:

- Fifty-four percent of executives surveyed believe the U.S. economy will improve in 2011—the highest rate of such optimism recorded since 2006.

- Thirty percent of companies plan to relocate workers this year—the highest percentage in six years.

- Eighty-seven percent of companies will spend as much or more on relocation in 2011 as in 2010—the most since 2007.

- The Midwest is now the top destination of transfers (37%) followed by the Northeast (31%), the South (28%) and West (20%).

And, please remember, I would be honored to serve as your Broker for all of your residential real estate needs. I want to help you, my reader, make the most prudent and accurate Real Estate business decision.

Also if you know of anyone who desires to buy or sell local real estate, or, who is moving in or out of the Pikes Peak region, remember that, with over 39 years of providing relocation and Real Estate services to clients throughout the country, I am uniquely qualified to assist them with the relocation process, including buying and/or selling their homes on both ends of their move. Please allow me to implement my negotiating skills on your behalf.

Just click on the icon at the top of this email to listen to my latest podcast. ….And, if you would like to learn more about our Job Loss Protection Program, please contact us.

LATEST STATISTICS

Click here for the latest Sales and Listing statistics for the Pikes Peak area

JOKE OF THE WEEK

On a road through a desert in Arizona, a preacher named Nathaniel Evans walked every day, preaching to the many people who roared past in their cars

"Repent, the End of the World is Nigh!" was his constant theme.

One day, as he was walking, he came to a big lever in the middle of nowhere, just by the side of the road. 'Pull this to end the world' said the sign on it.

Now Nathaniel saw this as the perfect spot for him to preach, and soon many automobiles were parked nearby, the people all swayed by his powerful elocution.

All was well, until there were so many people, and so many cars, that the road was nearly blocked. Then a big 18-wheel rig came down the highway, and couldn't stop in time. The driver had a choice: run over Nathaniel, or run over the Lever.

As the driver explained to the Highway Patrol later, he actually had no choice. Pointing to the red smear on the road that used to be Nathaniel Evans, he said "Better Nate than Lever."